[Disclosure: AgFunderNews’ parent company is AgFunder.]

Looking at the top-funded agrifoodtech startups in Africa in 2024, one recognizes several familiar names, including SunCulture, Apollo Agriculture, Tomato Jos, and Pula Advisors. Turning to 2023 fundraising, and you’ll see some of those names again along with a few other darlings of African agrifoodtech, including Hello Tractor and Twiga Foods.

“If you look at the list of companies that have raised the most funds, it would have been mostly the same list two years ago, three years ago,” says Maurice Scheepens, who leads the ventures program for agritech at Dutch entrepreneurial development bank FMO.

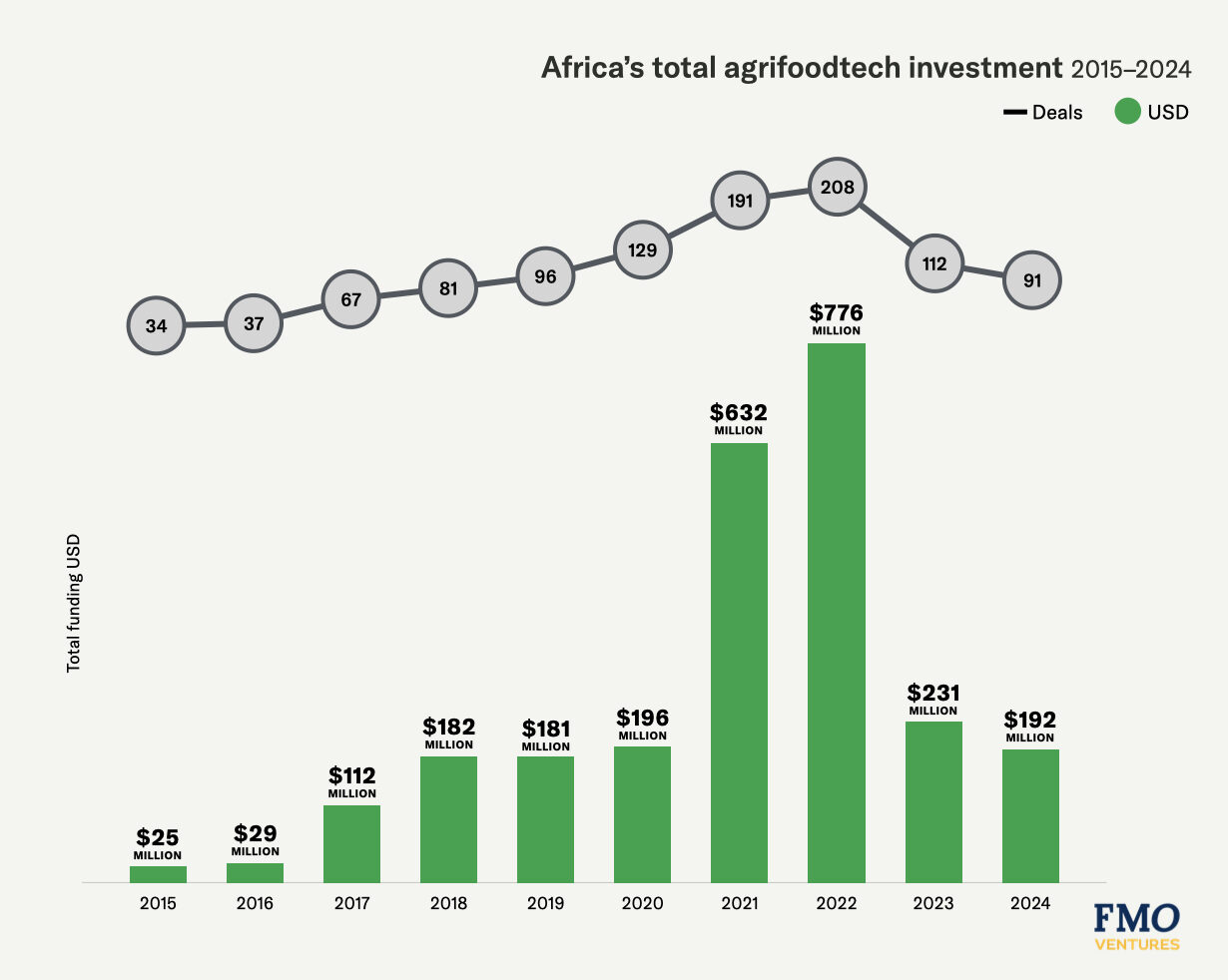

Most of these startups are based in Kenya, Egypt or Nigeria. Led by these ecosystems, funding to African agrifoodtech startups soared to record levels in 2022 ($776 million) and remain at pre-Covid levels with $192 million in 2024—more than 600% higher than 10 years ago, according to AgFunder’s recent Developing Markets AgriFoodTech Investment report. [Disclosure: FMO is a sponsor of AgFunder’s research.]

Africa agrifoodtech investment over time. Source: AgFunder Developing Markets AgriFoodTech Investment Report 2025

Africa agrifoodtech investment over time. Source: AgFunder Developing Markets AgriFoodTech Investment Report 2025

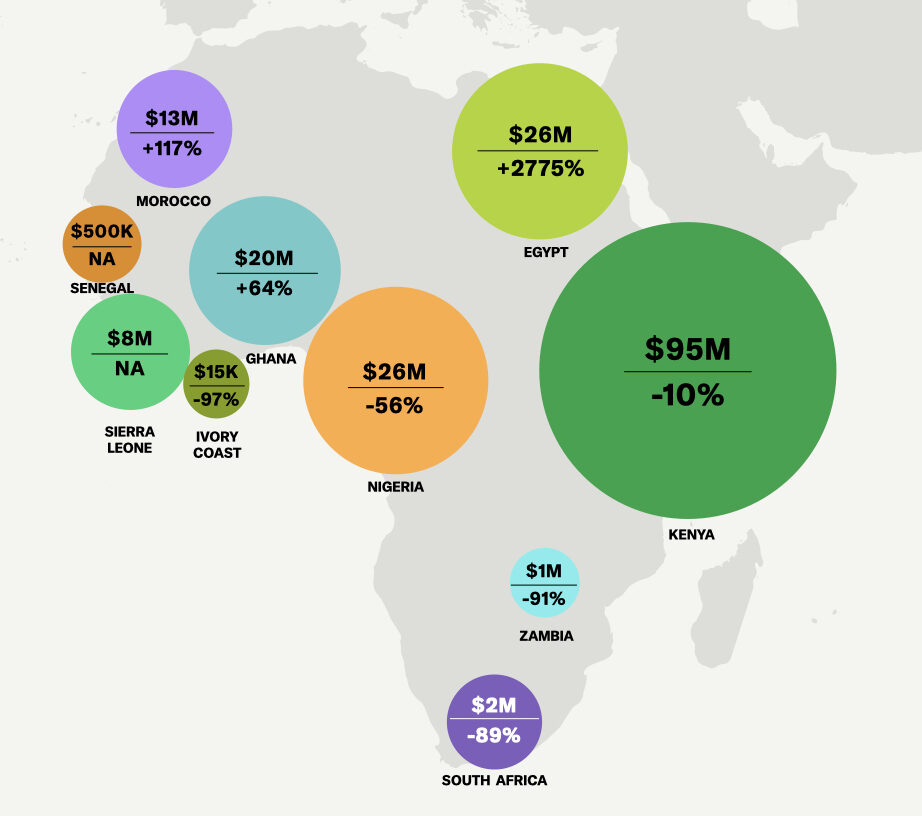

That Kenya, Egypt and Nigeria are leading the pack is not surprising when you look at the size of their economies and populations.

According to the World Bank, Nigeria has a population of 228 million and GDP of $364 billion. Egypt is close behind with 114 million and $396 billion GDP, while Kenya is 55 million strong with a GDP of $108 billion. These countries boast large populations of smallholder farmers too: 38 million, 24 million, and nearly 8 million, respectively.

However, as those darlings of African agrifoodtech mature, the big question is, when will the next wave of African agrifoodtech startups emerge? And more importantly, will new startups be able to thrive at a time when uncertainty and doubt have cast long shadows over the global economy and agrifoodtech investment continues to decline?

Africa agrifoodtech investment by country 2024. Source: AgFunder Developing Markets AgriFoodTech Investment Report 2025

Africa agrifoodtech investment by country 2024. Source: AgFunder Developing Markets AgriFoodTech Investment Report 2025

Looking beyond the obvious markets

FMO “deliberately” looks for opportunities beyond those core markets, despite their relative size, says Scheepens.

Ghana, the fourth-most-funded African country in 2024 (for agrifoodtech), has a population of 34 million and GDP of $76 billion. Likewise, Morocco is home to 38 million and has a $144 billion GDP. The number of farmers for these countries are substantially lower: 7 million in Ghana and less than 4 million in Morocco.

Scheepens explains that for Nairobi-based investors, it’s easier to look at Kenya first before looking at Uganda or another country; the same applies to Nigeria, which serves as the hub for West Africa.

“So there’s a lot of liquidity in these markets,” Scheepens says. “There’s already ample investment appetite in those places, and we try to seek out companies that have equally interesting opportunities or theses, but have less availability of capital.”

For example, FMO participated in Yola Fresh’s $7 million pre-Series A round in 2024, a Morocco-based platform that streamlines the market linkage between farmers and consumers. In the same year, it also invested in food distribution network East Africa Foods (“EA Foods”), based in Tanzania.

Elsewhere, its partnership with Endeavor aims to provide greater support to agrifoodtech startups on the continent by helping them build strong business models that are attractive to investors.

“We have a robust and diverse pipeline of emerging agtech startups, sourced through multiple channels from team members deeply embedded in West, East and Southern African ecosystems,” says Toffene Kama, principal investor at Mercy Corps Ventures, the investment arm of humanitarian organization Mercy Corps.

While that includes some of the African agrifoodtech “darlings,” like Kenya’s Wasoko, investments also go beyond the big three, as with Ghana-based ag marketplace Complete Farmer, which secured a $10 million Series A round in 2024.

“We were the first investors in Pula, Wasako (which merged with MaxAB), and early investors in Complete Farmer,” adds Dan Block, an investment partner at Mercy Corps Ventures.

“Some of the next generation of agtech leaders we’ve backed are really focused on the first mile/last mile data layer challenges and opportunities for precision ag, supply chain orchestration, soil health, and traceability,” he says.

Mercy Corps ventures has recently invested in precision ag company Tolbi, from Senegal; Tanzania-based farm software startup MazaoHub; Ghana-based weather forecasting innovator Ignitia; and supply chain-focused companies Agrails and Meridia, which operate in multiple markets in East Africa and West Africa, respectively.

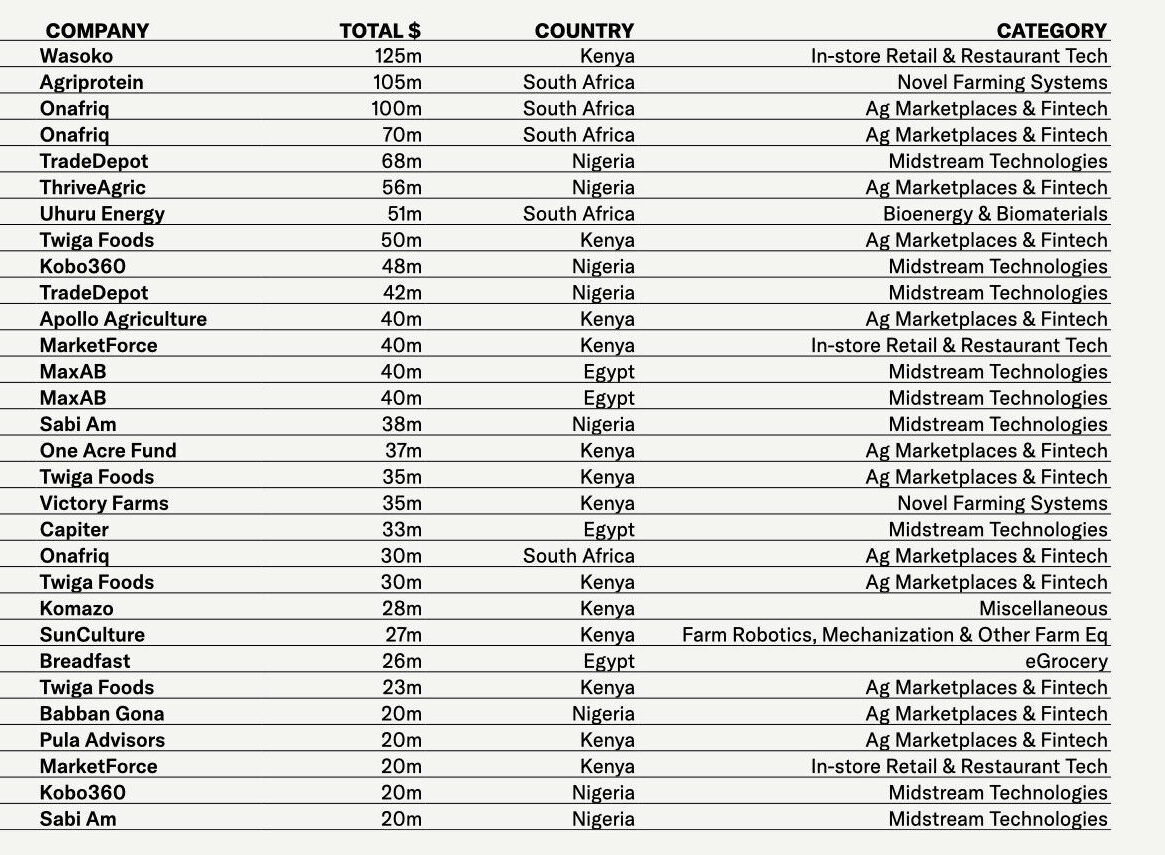

African agrifoodtech’s top 30 rounds since 2012

Source: AgFunder Developing Markets AgriFoodTech Investment Report 2025

Source: AgFunder Developing Markets AgriFoodTech Investment Report 2025

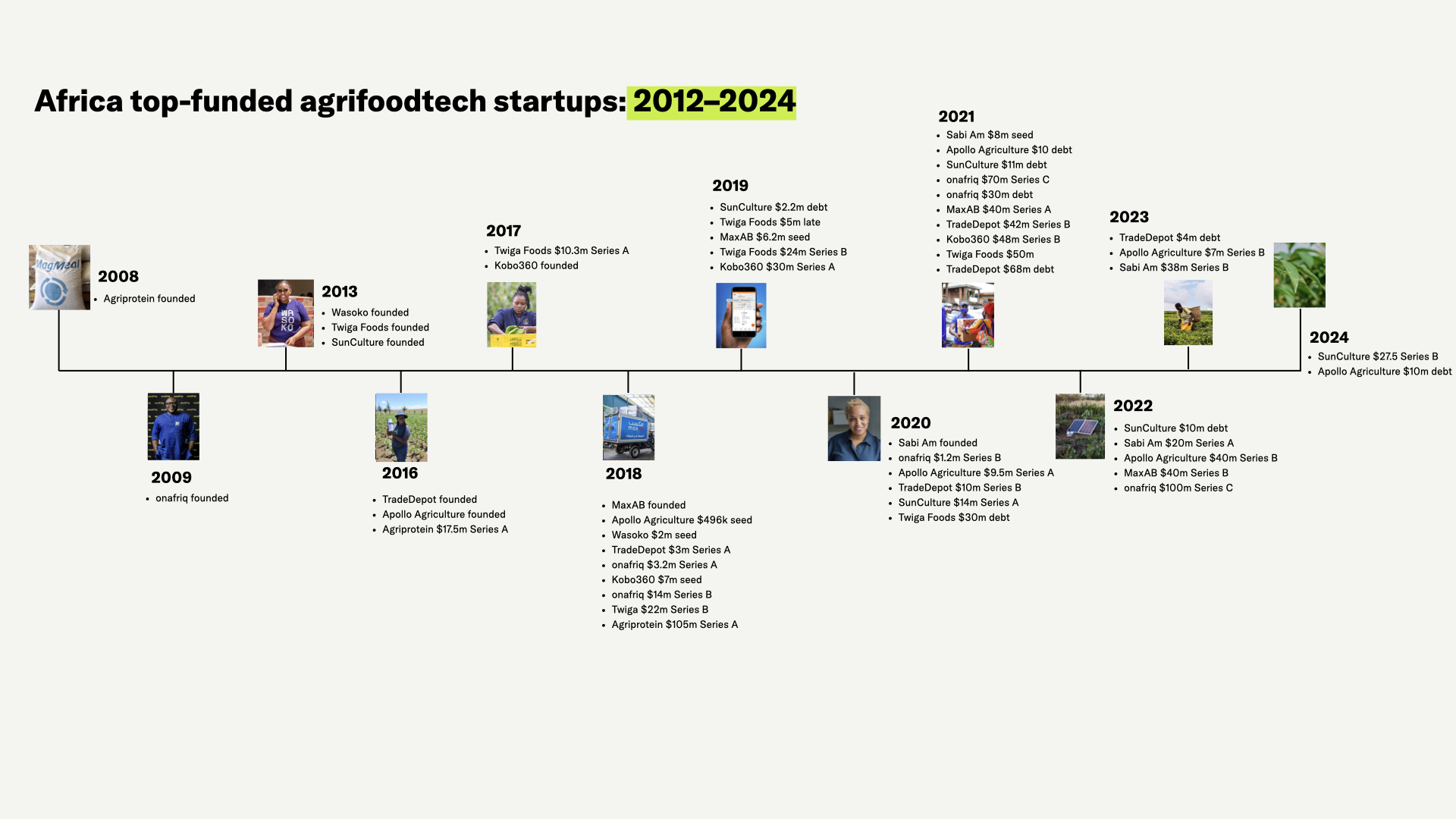

A timeline of funding rounds for Africa’s top 10 best-funded startups since 2012. Image credit: AgFunderNews

A timeline of funding rounds for Africa’s top 10 best-funded startups since 2012. Image credit: AgFunderNews

‘We need more sector-specific funds’

The key to finding and sustaining the next generation of African agrifoodtech startups is to address problems in agriculture that are specific to Africa, says Sherief Kesseba, managing partner for the Climate Resilient Africa fund (CRAF).

“We need more sector-specific funds that can lead rounds and validate opportunities. Agrifood funds that understand the space and that can spot the sustainable solutions that are addressing real African food system problems.”

To that end, CRAF’s portfolio is heavily focused on categories such as Ag Marketplaces and Midstream Technologies (ie., the supply chain).

Nigeria’s Winich Farms links smallholder farmers to financial services and markets, for example. Sea Gardner in Egypt operates a distribution network for delivering shellfish live to customers. Uganda’s Munakyalo Agrofresh provides solar-powered innovations to reduce post-harvest losses among smallholder farming communities.

“At the moment, generalist/sector-agnostic funds await more advanced rounds (raising bigger tickets at higher valuations) as they somewhat provide a de-risking of the opportunity,” says Kesseba.

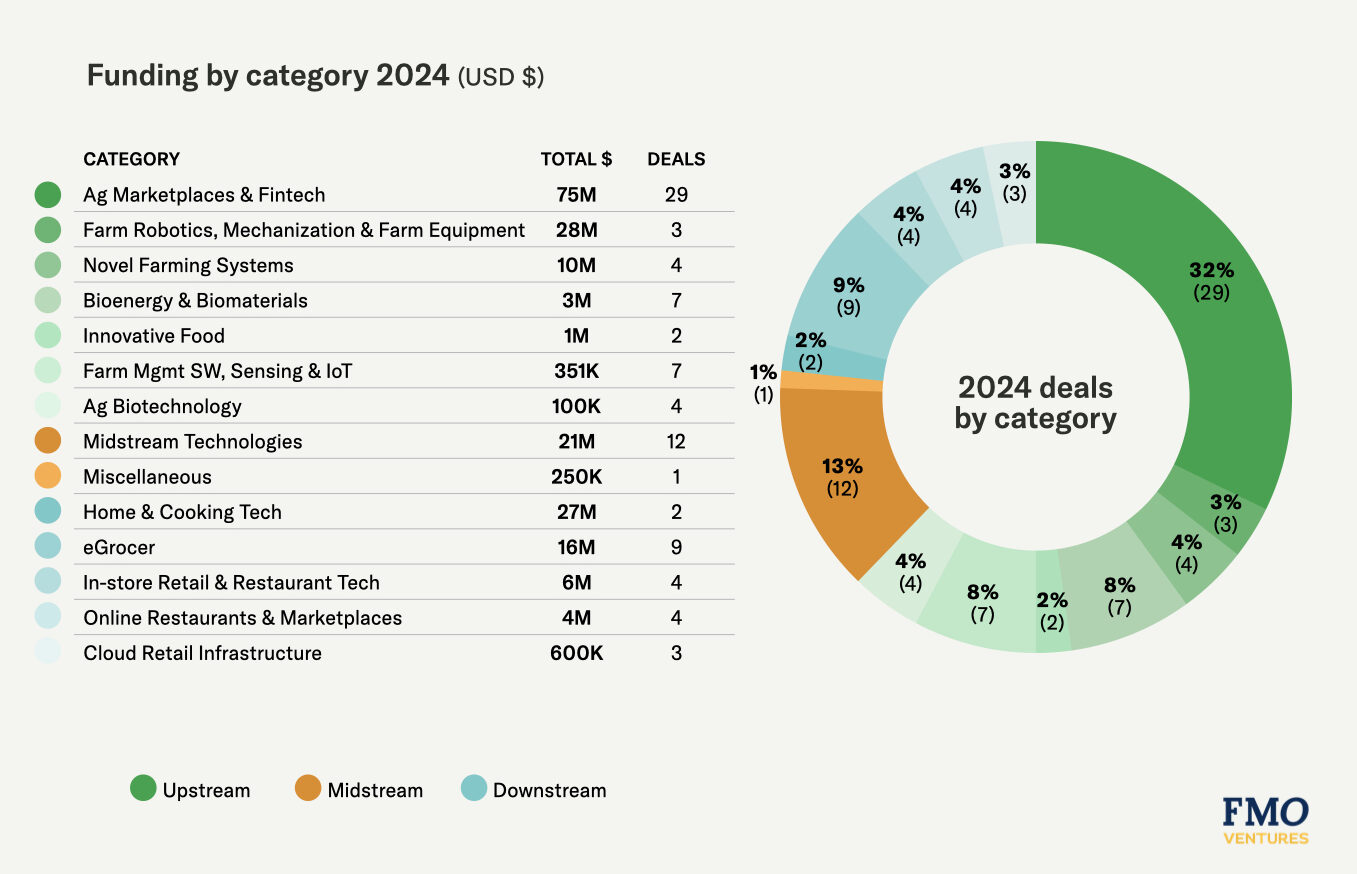

Africa agrifoodtech funding by category 2024. Source: AgFunder Developing Markets AgriFoodTech Investment Report 2025

Africa agrifoodtech funding by category 2024. Source: AgFunder Developing Markets AgriFoodTech Investment Report 2025

‘The building blocks’ of African agrifoodtech

For the foreseeable future, Africa’s top investment categories are likely to remain Ag Marketplaces & Fintech, and Midstream Technologies.

“These are the building blocks of our very nascent ecosystem as these solutions allow for penetration into the SHF [smallholder farmer] base who are responsible for 80+% of the African food system,” says Kesseba.

“Marketplaces and Midstream innovations allow for SHFs to be effectively clustered and digitized, allowing for economies of scale that open the door to being able to serve them and help them access credit, insurance, inputs/machinery, markets etc. This enables them to transition away from subsistence farming and into commercial farming.”

Ag Marketplaces are a prime example of “tech-enabled” models, says Scheepens, where the emphasis is not on “high tech” but on tech that can enable more efficiency.

“Tech-enabled models are where we try to make supply chains more efficient, allow farmers to get access to better quality inputs or knowledge, and link them to markets,” he says.

Oftentimes this results in a marketplace startup evolving its business model into brick-and-mortar services, such as storage and transport, to ensure the success of the overall platform. This even stretches to training and on-the-ground advisory.

Social enterprise WARC, based in Ghana and Sierra Leone, operates a low-tech trading operation that relies on physical “trading hubs” to connect farmers with buyers and input suppliers. Technology plays a role in this connection but is not the main focal point of its community hubs or its on-the-ground training. The company raised a $7.5m Series B round in 2024.

Apollo Agriculture, one of Africa’s most successful agtech startups, which raised 2024’s second-largest Ag Marketplace deal at $10 million, provides credit to farmers to purchase inputs from some 1,000+ agrodealers in its network and insurance, but also “best-in-class agricultural training.”

Yet Apollo and Pula Advisors, the ag insurtech startup that raised the year’s biggest Ag Marketplace round with a $20 million Series B, are among the category’s most high-tech. Both use sophisticated machine learning models based on a variety of data sources from satellite imagery to transaction data to asses a farmer’s creditworthiness, in Apollo’s case, or model out insurance risks for Pula.

WARC Africa is a social enterprise connecting farmers to buyers and input manufacturers. Image credit: WARC

WARC Africa is a social enterprise connecting farmers to buyers and input manufacturers. Image credit: WARC

Investing in ‘the specifics’ of African agrifoodtech

All that said, “Ag Marketplaces” and “Midstream Technologies” are broad categories. As such, Kama advocates for “immersing” oneself in the nuances of specific agtech subsectors.

For example, solutions that reduce post-harvest loss—which impacts 20% to 40% of crops in sub-Saharan Africa—address one small area of the overall supply chain, which is often riddled with inefficiencies for smallholder farmers.

“This loss occurs after months of labor and input investment, meaning massive inefficiencies and direct income losses for smallholder farmers,” he says.

Other areas to keep an eye on include precision agriculture, which promotes remote sensing and AI to eliminate guesswork in agricultural production, and data-based solutions that boost traceability.

The latter is particularly important for African producers in light of the EU Deforestation Regulation (EUDR) law, which requires that products like cocoa, coffee, palm oil, and soy sold into Europe be traceable to the exact plot of land where they were grown, says Kama.

“Data about how and where a crop is produced will become just as critical as the crop itself.”

A deeper understanding of sub-sectors shapes investment decisions, he adds.

“We believe the next generation of African foodtech will be shaped by startups that specialize narrowly—whether in input provision and financing, production, post-harvest handling and storage, or market access.

This is in contrast to earlier ventures that often attempted to build “end-to-end” platforms but were unable to scale thanks to fragmentation of the ag value chain in Africa, he notes.

“In contrast, startups that begin with unique tech capabilities in a focused niche can gain traction faster, build strong early customer bases, and grow through strategic partnerships across the rest of the chain.”

For more in-depth research about African agrifoodtech and other developing markets, check out AgFunder’s research here.

The post Where will the next darlings of African agrifoodtech come from? appeared first on AgFunderNews.